4 alternatives to savings certificates

If you're thinking of diversifying your investments, discover 4 alternatives to savings certificates.

Savings certificates are a traditional way of saving in Portugal, but there are many other options to explore. Have a look at what they are and whether they are a good alternative to savings certificates for you.

What are savings certificates?

Savings certificates are government-issued savings products aimed at small investors looking for a safe and affordable way to invest their money. These certificates are guaranteed by the government itself, making them an attractive option for those who want to save without taking on huge risks. In addition, savings certificates offer an interest rate that is updated quarterly and interest that is automatically capitalised, allowing investors to benefit from stable returns over time.

The perpetuity premium is added to the basic interest rate from the 2nd year onwards, as follows:

• 0.25 % – from year 2 to year 5;

• 0.50 % – from year 6 to year 9;

• 1.00 % – in year 10 and year 11;

• 1.50 % – in year 12 and year 13;

• 1.75% – in year 14.º and year 15;

Keep in mind that the base rate cannot be lower than 0% or higher than 2.5%.

Advantages:

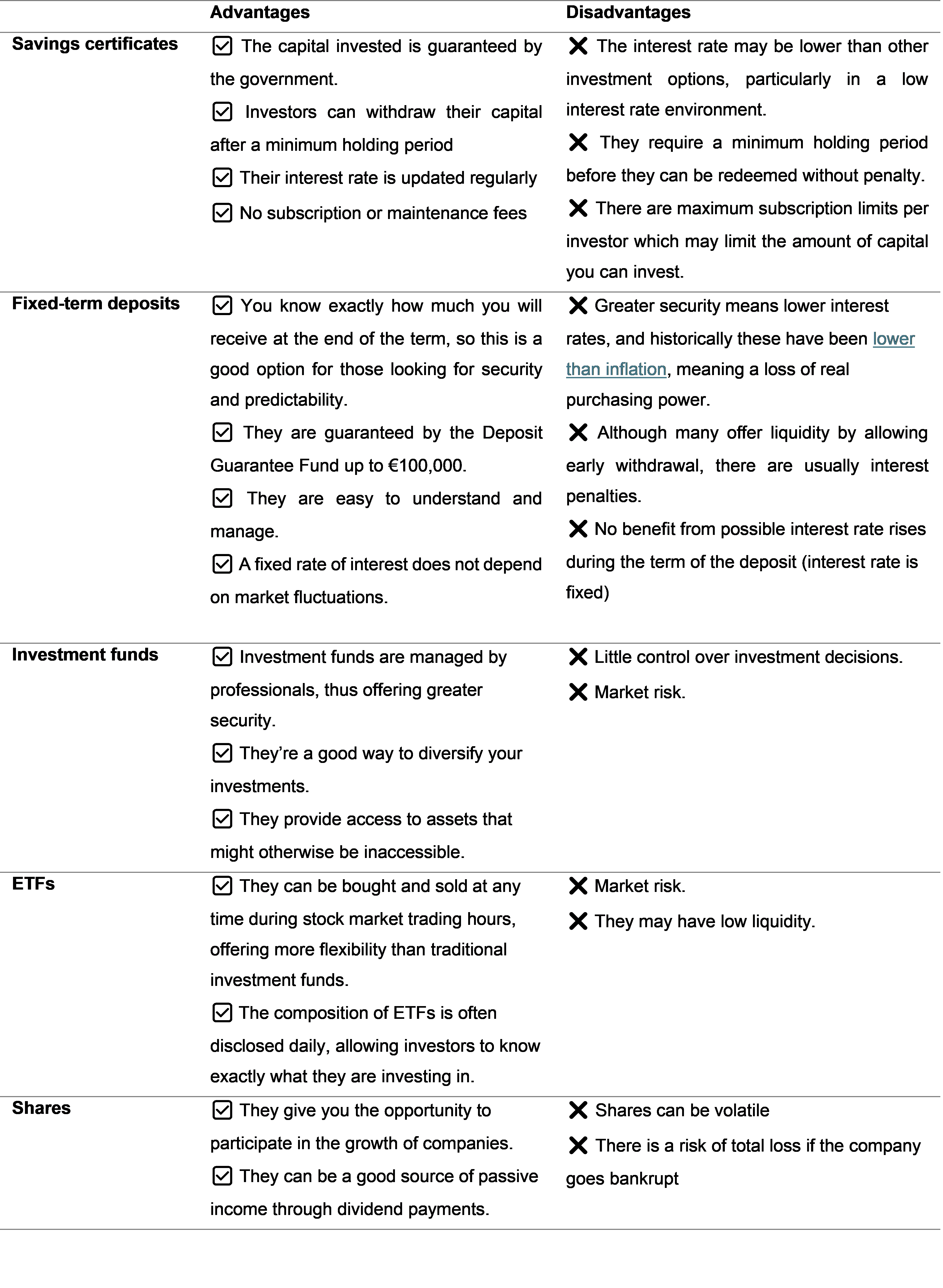

• The capital invested is guaranteed by the government;

• Investors can recoup capital after a minimum holding period;

• Their interest rate is updated regularly;

• No subscription or maintenance fees.

Disadvantages:

• The interest rate may be lower than other investment options, particularly in a low interest rate environment;

• They require a minimum holding period before they can be redeemed without a penalty;

• There are maximum subscription limits per investor which may limit the amount of capital you can invest.

Conclusion:

Savings certificates are an option for investors looking for security and stability in their investments. Guaranteed by the government, they offer a safe way to save, with the added benefits of an interest rate that is boosted by loyalty bonuses and some ease of redemption. However, the relatively low interest rate and the minimum duration are aspects to be taken into account.

Alternatives to savings certificates

Here are 4 alternatives to savings certificates you need to know about.

1. Fixed-term deposits

Fixed-term deposits are one of the simplest and safest forms of investment. The interest rate is agreed at the outset and generally the longer the term, the higher the rate.

Advantages:

• You know exactly how much you will receive at the end of the term, so this is a good option for those looking for security and predictability;

• They are guaranteed by the Deposit Guarantee Fund up to €100,000;

• They are easy to understand and manage;

• A fixed rate of interest does not depend on market fluctuations.

Disadvantages:

• Greater security means lower interest rates, and historically these have been lower than inflation, meaning a loss of real purchasing power;

• Although many offer liquidity by allowing early withdrawal, there are usually interest penalties;

• No benefit from possible interest rate rises during the term of the deposit (interest rate is fixed).

Conclusion:

Fixed-term deposits offer an attractive combination of simplicity and security, making them a solid option for investors who value predictability and want to protect their capital. They complement a savings and investment strategy.

2. Investment funds

Investment funds are financial vehicles that pool the capital of several investors under a professional manager. These funds may invest in a variety of assets, such as shares, bonds, property and others, in accordance with the defined investment policy.

There are investment options that provide exposure to the financial markets, increasing returns but with a lower level of risk for investors with a more conservative profile. Alternatives include bond funds and money market funds.

Advantages

• Diversification: Investment funds allow diversification, reducing the risk associated with any single asset;

• Professional management: Funds are managed by experienced professionals, which can benefit investors who don’t have the knowledge or the time;

• Accessibility: Funds provide access to a wide range of assets that might otherwise be inaccessible to retail investors;

• Adjusted risk level: Investment funds have a risk level (from 1 to 7) that allows investors to assess whether the risk of this investment is in line with their objectives;

• Subscription and redemption at NAV: Unlike ETFs, in many cases there are no entry or exit fees for subscribing to investment funds (although there may be some, so you should check the terms and conditions of each fund before subscribing).

Disadvantages:

• Lack of control: The investor has little control over investment decisions, depending on the fund manager. However, in most cases you can easily redeem your investment.

• Market risks: Although investment funds are diversified, they are not risk-free and may suffer losses. It is important to remember that they are not guaranteed capital instruments.

Conclusion:

Investment funds are an option for investors seeking diversification and professional management, as long as they are managed by an experienced team with a proven track record of performance.3. ETFsETFs are investment funds that are traded on the stock exchange in a similar way to shares. They are best known for tracking the performance of a market index, such as the S&P 500, which allows investors to gain exposure to the movements of all the stocks that make up the index by buying just one ETF. However, unlike savings certificates and investment funds, they do not have a guaranteed principal.

Advantages:

• Trading flexibility: can be bought and sold at any time during stock market trading hours, offering more flexibility than traditional investment funds;

• Accessibility: Funds provide access to a variety of assets that may otherwise be inaccessible to retail investors;

• Transparency: The composition of ETFs is often disclosed, allowing investors to know exactly what they are investing in.

Disadvantages:

• Market risk: Like other investments, ETFs are subject to market risk and may lose value;

• Liquidity: Some ETFs may have low liquidity, which can make it difficult to buy or sell at the desired prices;

• Trading costs: As exchange-traded instruments, transactions in ETFs may be subject to transaction costs such as exchange fees, commissions and the difference between the buy and sell market prices.

Conclusion:

ETFs are an option for those seeking exposure to a broad range of assets or market indices. However, it is important to consider the liquidity and market risk involved.

4. Shares

Shares represent a stake in the share capital of a company, which gives the shareholder the right to receive a share of the profits (dividends). In some cases, they may entitle the holder to participate in decision-making by voting at general meetings. Unlike savings certificates, shares do not offer a guaranteed principal.

Advantages:

• Potential return: Shares can provide returns through capital appreciation;

• Dividends: Some companies pay out part of their profits in the form of dividends, which can be a good source of passive income.

Disadvantages:

• Volatility: Shares can be volatile, with prices rising and falling rapidly;

• Risk of total loss: If the company goes bankrupt, the shareholder could lose all the capital invested.

Conclusion:

Investing in shares gives you the opportunity to participate in the growth of companies and receive income through dividends. However, it is important to be aware of the risks involved and to consider a long-term strategy, especially when choosing shares in stable, dividend-paying companies.

Conclusion: are savings certificates worth it?

Key Takeaways

What are Savings Certificates and how do they work?

Savings Certificates are state-issued savings products in Portugal, offering guaranteed capital and automatically capitalized interest. With quarterly updated rates and loyalty premiums, they suit investors seeking stability.

What are the best alternatives to Savings Certificates?

Key alternatives include:

- Term deposits – secure, with fixed rates;

- Investment funds – diversified, professionally managed;

- ETFs – flexible, traded on exchanges;

- Stocks – potential for capital gains and dividends.

What are the risks of alternatives to Savings Certificates?

Risks vary:

- Term deposits: low returns, penalties for early withdrawal;

- Funds and ETFs: market risks, no capital guarantee;

- Stocks: high volatility, potential total loss.

Assess your risk tolerance before investing.

How do I choose the best alternative to Savings Certificates?

Consider:

- Financial goals and risk tolerance;

- Liquidity and investment horizons;

- Professional management, like that offered by Banco Carregosa;

- Diversification to mitigate market risks.

Banco Carregosa, helping you make the best investment decisions