US inflation outlook in line with economic growth developments.

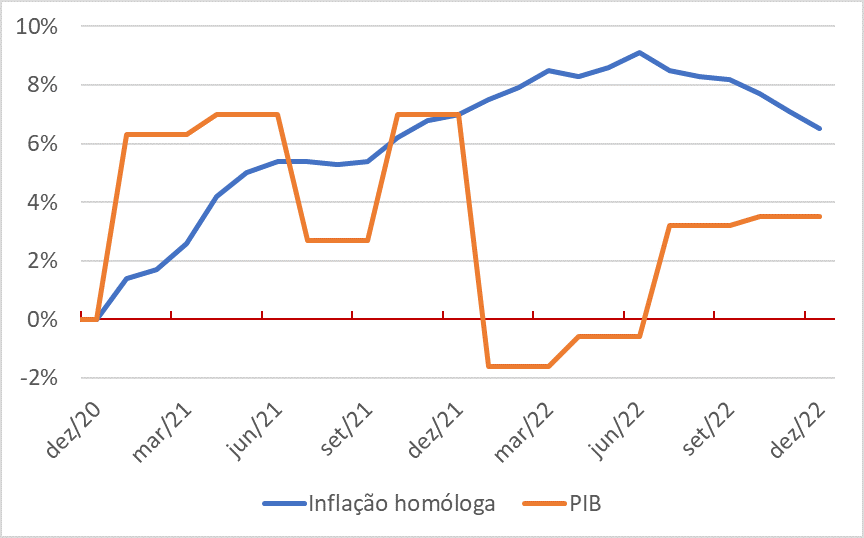

US year-on-year inflation slowed in the second half of last year, with the Consumer Price Index (CPI) rising by only 0.2% between June and December 2022, mainly due to improvements in the supply chain. The gradual narrowing of the US trade deficit from April last year boosted economic growth in the second half of the year, after a contraction in the first half. The US economy contracted by 1.6% and 0.6% respectively in the first and second quarters of last year (see Chart 1). The US economy grew by 3.2% in the third quarter and is expected to grow by 3.5% in the fourth quarter, according to the Atlanta Fed's GDP Now data on 18 January. Chart 1 shows the inverse correlation between the inflation rate and the economic growth rate. While inflation gradually increased throughout 2021 and into the first half of 2022, the economy slowed down and even contracted in the first half of last year, but the downward trend in the unemployment rate continued, reaching full employment still in the first quarter of 2022, which does not confirm the classical Phillips curve. Meanwhile, the slowdown in inflation from June 2022 onwards coincided with the economic recovery in North America.

Chart 1 – Developments in inflation and GDP in the US over the past 2 years

Source: Banco Carregosa, Bloomberg and Atlanta Federal Reserve

The improvement on the supply side has allowed for higher economic growth and a fall in inflation, which is the most favourable scenario for the rise in equities that has been observed since the beginning of October last year with the general recovery in the equity markets. However, the highly restrictive monetary policy introduced by the US Federal Reserve (Fed) almost a year ago is threatening economic growth, gradually affecting the ability to finance future investment due to higher interest rates, and also penalising the financing of indebted families and companies as loans are renewed, now at much higher interest rates.

Demand, which still resilient largely due to savings from pandemic and containment support, could gradually be penalised in the coming months as rising interest rates erode disposable income, threatening business sales and economic growth.

As interest rates remain high for longer, not only the likelihood of a recession but also its depth increases. If there is a recession, inflation could drop towards the Fed's price stability target. This scenario of low inflation and recession is positive for sovereign bonds.

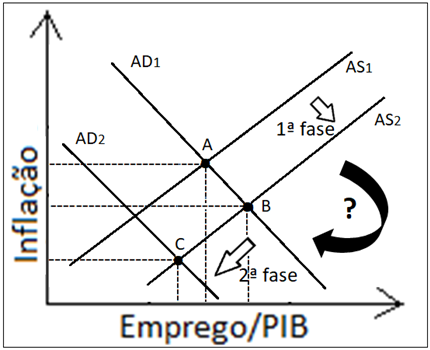

Charts 2 and 3 show the scenarios of improving inflation, in a first phase due to the gradual fading of difficulties in supply chains, GDP growth and a robust labour market (deflationary boom), and in a second phase of continuously falling inflation, but in this case in a recessionary context (deflationary bust).

Chart 2 – Inflation and GDP developments

Source: Banco Carregosa

In a first phase, the increase in aggregate supply (AS1 to AS2) allows inflation to fall in an environment of economic growth (point A to point B). However, progressively higher interest rates penalise aggregate demand (AD1 to AD2), increasing the likelihood of a recession and a rise in the unemployment rate. This scenario could be beneficial for significantly lower inflation, but in a recessionary environment (now from point B to point C). In its last report in December, the Fed expected the unemployment rate to rise to 4.6% by 2023, but it still expects the economy to growth by 0.5% this year, albeit at a slower pace. Currently, the US unemployment rate stood at 3.5% in December and the year-on-year inflation rate has fallen to 6.5%.

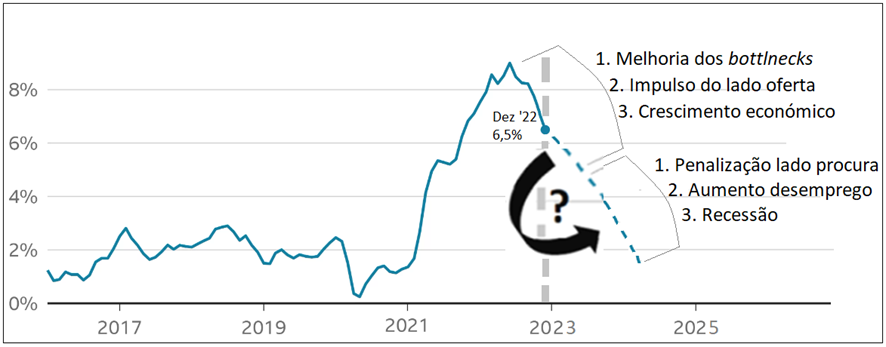

Chart 3 – Annual inflation developments in the USA (backward- and forward-looking)

Source: Banco Carregosa

The Fed is keen to get interest rates back to the 2% target, but the question is whether it can do so with a soft or a hard landing of the economy. Meanwhile, US inflation data for December showed resilience in the shelter category (rents and equivalent homeowner rents), which continues to drive inflation and accounts for a third of the Consumer Price Index (CPI).

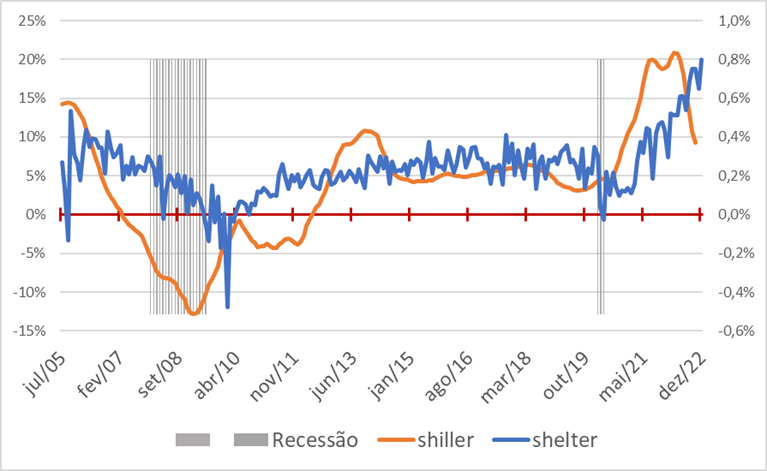

Chart 4 - US house price (shiller) and shelter CPI developments

Source: Banco Carregosa, Bloomberg

Chart 4 shows that the shelter item lags house price changes by 12 to 18 months, and in recessions the growth of the shelter item is zero or even negative. It currently accounts for around 3 percentage points of the 6.5% US CPI in December, or almost half of current inflation. It is a significant burden that has been pushing up inflation, but as house prices slow, the downward adjustment tends to occur and can be accelerated in a recession.